Micro-Loans: YOU may be Eligible

Micro-Loans: YOU may be Eligible

Reminder that qualifed readers can GET as well as GIVE, zero-interest microloans!

No-Interest, No-fee, Non-profit Microloans for US micro-preneurs and small businesses!

Most of you already know that 100% of our paid subscription fees go to helping micro-preneurs looking to enter the “parallel economy” launch and gain freedom, autonomy and opportunity. However..

What you may not realize is that YOU too can avail yourself of this service providing you match the criteria.

The team we run only offers one type of financing: microloans. Our loans go up to $15,000.

(Btw STNN Readers. Here’s where 100% of your money goes when you become a paid subscriber! Thank you!):

If that number worries you, then a small loan from Kiva (the only kind it offers) is probably not for you. Because remember, that’s the maximum loan size. In other words, your microloan could be smaller.

But maybe you just need a small amount of working capital to renovate your bakery’s kitchen, add more inventory, pay for a training program, or start an online sales or consulting service.

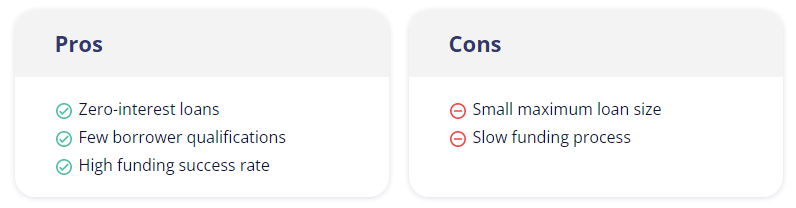

In that case, we may well be your best choice for microloans, thanks mostly to zero-interest and no-fees. That’s right―Our STNN team (through US Kiva) doesn’t charge any interest on its small-business loans. And, well, you can’t find a better deal than that.

There’s a really good chance that you qualify for one of these loans. K.USA doesn’t look for a specific credit score or revenue amount. Instead, it sticks to a few simple borrower requirements:

Must live in the US (but not Nevada, New Mexico, North Dakota, Rhode Island, or Vermont)

Must be at least 18 years old

Must use loan for business reasons, not personal ones

Can’t have any active bankruptcies, foreclosures, or liens

And that’s pretty much it. Kiva will still look at how long you’ve been in business, your revenue, and other factors to decide what size loan you get. But you won’t be disqualified because of any of those factors.

If all that weren’t enough, Kiva claims that more than 90% of would-be borrowers get funded. That’s an amazingly high rate.

That doesn’t mean that such a microloan will work for all businesses, though. So before you start that loan application, let’s talk about the funding process.

Kiva doesn’t lend money itself. (In fact, it’s a nonprofit organization, not a lender.) Instead, Kiva sits somewhere between crowdfunding and peer-to-peer lending. You create a campaign, people pledge money to your campaign, and then you repay the money you get.

This process is what lets Kiva make such affordable loans―but it also makes the funding process take a fairly long time.

It all starts with your application.

Applying for a Microloan

You’ll start out by submitting an application (see link further down)

Keep in mind, this application isn’t at all like the ones you’ll find from most online lenders. While other lenders try to keep things as quick and simple as possible, Kiva really wants to dig into you and your business or new business idea.

So after you answer some basic questions, you’ll have to write some detailed paragraphs about yourself, your business, and why you need a microloan. You’ll submit that, plus a photo of yourself with your business. (Take your time with this part, as it will all be in your loan profile later and it no doubt affects which loans others are inclined to support. Hint, you want to look positive, competent, friendly and trustworthy)

And then you wait.

A Kiva representative will get back to you about your application, but this can take between 10 and 15 days. They may ask you some more questions, and they’ll help you set an appropriate fundraising goal. Once your rep is satisfied that everything looks good, they’ll approve your application.

That doesn’t mean you get money right away, though. Instead, it means you get to start fundraising.

Raising money

To prove your creditworthiness, you have to start your fundraising period by getting family and friends to contribute. They can offer as little as $25, but you have to invite between 5 and 35 people to contribute. (The exact number of people will depend on a few different factors, including your loan size.) You’ll have 15 days to meet this goal.

Once you’ve gotten those people to contribute, you can take the campaign public. Your profile will get listed on Kiva’s crowdfunding platform, and anyone can offer money. This part will last up to 30 days or until you meet your funding goal―whichever comes first.

With any luck (and some marketing work on your end), you’ll meet your loan goal and be able to get funding.

Getting and repaying your loan

About a week after your campaign ends, Kiva will use PayPal to get you your loan funds. (Note that you will need a business bank account for this bit.)

One month after that, you’ll start making payments. Again, these payments will go through PayPal. And Kiva doesn’t automatically take payments like other lenders do. You’ll have to manually make your payments, so make sure you set a reminder for yourself.

When all is said and done, it can take more than two months to get a Kiva microloan. That’s, well, a really long time―especially when you can get fast and easy business loans that offer same-day or next-day funding.

But is it worth it? Let’s look closer at Kiva's microloans to find out.

Kiva loan options

As we mentioned earlier, Kiva offers only one type of financing. Its microloan comes in different amounts with different repayment terms, but they’re all the same product.

Kiva financing

Product

Min./max. loan size

Interest rate

Repayment terms

Learn more

Kiva microloan$1,000/$15,0000%12–36 mos.See Loan Offers

Data effective 12/8/22. At publishing time, pricing is current but subject to change. Offers may not be available in all areas.

Your exact microloan amount will depend on factors like how much debt you have and how much revenue you earn. For reference, the average Kiva microloan size is $5,000.1 (That may change, though, since Kiva recently raised its maximum loan size from $10,000 to $15,000.)

Smaller loans will come with a shorter repayment term. Only loans over $6,500 qualify for a full three-year term. While terms of one to three years aren’t super long, they’re pretty standard for microloans. In other words, Kiva offers competitive repayment terms.

But as we’ve already said, the real selling point of Kiva’s microloan is the 0% interest rate. You simply can’t beat that.

Kiva doesn’t charge any fees either. So when you get a $5,000 loan, you actually get the full five grand―not $5,000 minus an origination fee, like you’d get from many lenders.

Kiva success rates

According to Kiva, more than 90% of business owners manage to get their microloan funded through Kiva.1 That’s a higher rate than we’ve seen on any other crowdfunding platform.

But it’s worth taking a minute to break down that success rate further.

As you’ve probably already realized, it’s Kiva’s mission to get loans into underserved communities. This is a big problem in business lending. Some groups, like women and minority business owners, don’t have the same kind of financial access that other business owners do. In fact, they get turned down for loans at a much higher rate than business owners as a whole do.

Not so with Kiva. Of all Kiva borrowers, almost 70% are women business owners, and just over 70% are minority business owners.1 More than half of Kiva borrowers got rejected for business loans elsewhere.1

In other words, Kiva is successful not only at funding microloans, but at fulfilling its mission. So while it may be slow and cumbersome, we’re glad it’s providing loans to business owners who otherwise wouldn’t get them.

Kiva microloans stand on their own merits. They’ve got no interest or fees, and they come with lengthy repayment terms. So while you can only get a small loan from Kiva, it’s still one of the best deals in financing.

Just don’t expect to fund your business overnight. Kiva requires a long application and funding process. But if you’ve got the time, we think it’s worth it.

HERE’S WHERE THIS STACK COMES IN: We actively seek out and contribute to funding approved US-based loans from folks who follow this stack or inform us that they have a loan waiting to be fully funded. This can speed up the process exponentially! (note: Kiva in the US works quite differently than Kiva elsewhere in the world. The biggest difference? Outside of the US, Kiva loans through field partners, and borrowers have to pay interest to those partners. Not so here!)

IF YOU’D LIKE TO GET STARTED, YOU CAN

APPLY NOW: Crowdfund your Dream. Change your LIFE!

Click here to SEE IF YOU QUALIFY FOR A MICROLOAN!

*excerpted from No Interest, No Fee Microloans for US Businesses

https://www.business.org/finance/loans/kiva-review/

Here's one of our latest microloans, thanks to YOU!

https://www.kiva.org/invitedby/theflyingwallenders/for/2756659

You want to loan me 250 bucks so I can upgrade my paper cut art business with a laser cutter?